Regulations

When it comes to mortgage loan advertising, there are a couple regualtory bodies that have published their own regulations. These rules that all mortgage companies must live by can offer punitive penalties for not adhering to them. Penaties such as fines, license revocation, and restitution for harm that may have been caused as a result of misrepresented mortgage advertising. Some of these regulations include the Mortgage Acts and Practices-Advertising (MAP) Rule, published by the Federal Trade Commission (FTC), and the Truth in Lending Act (ACT) published by the Consumer Financial Protection Bureau (CFPB).

Truth in Lending (reg Z)

The Truth in Lending Act, also referred to as Reg Z, is the main source for what is and is not allowed when it comes to mortgage advertising. Reg Z was enacted to protect consumers from predatory lending practices and requires that mortgage lenders, or brokers, disclose borrowing costs, interest rates, and upfront fees written in clear language so that consumers can understand all of the terms that are associated with a mortgage loan and make informed decisions. Not only do advertisements need to be clear and concise, without masking or hiding certain limitations, but when the advertisements contain certain trigger terms, additional disclosures are required.

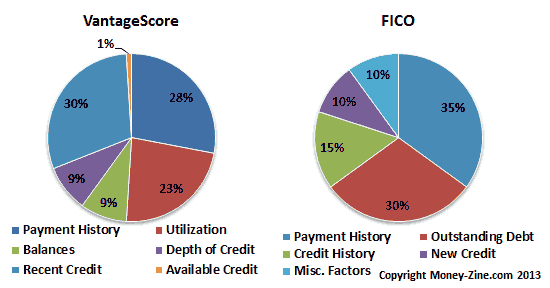

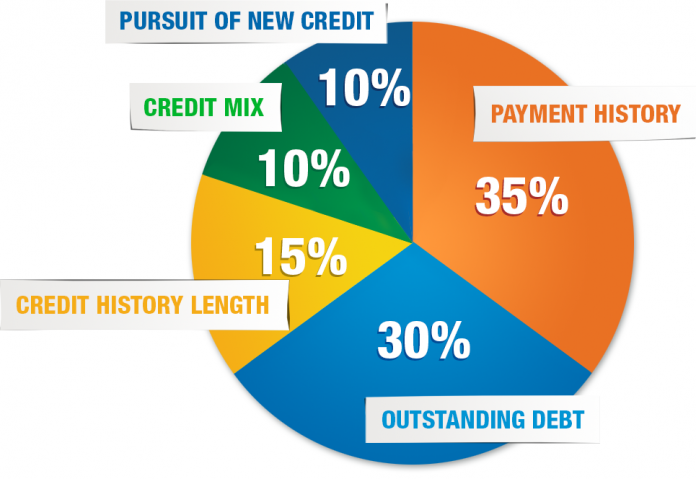

How to improve credit score

As mentioned briefly above, there are many ways to improve your score. Here are some pointers:

1. The first and most obvious way is to make on-time payment each month to your creditors. Understandably, sometimes a bill is forgotten or you just did not have the money to pay it that month. Do not let one month, where you may have slipped, destroy your payment rhythm.

2.Pay down your credit cards. Some sources believe that maintaining a balance of less than 30% is ideal.

3. When you start thinking of applying for a home loan, do not apply for new credit until the process is completed. This will lower your average age of credit as well as add inquiries to your credit.

4. If you have derogatory or collection accounts, look to pay them. Sometimes you can contact the creditor and arrange for them to remove the account from your credit completely once you have paid the arranged amount.