How does loan amount and credit score impact a home loan interest rate?

The loan amount and credit score typically get lumped together as risk and a negative or positive adjustment is applied to the rate. So for example, if you are qualified for a $4,000,000 loan (WOW! wouldn't that be crazy?) but your credit score is on the lower end, the lender may apply a positive adjustment to the rate based on the risk. Conversely, if you are applying for a $200,000 loan with a credit score on the higher side, the lender would apply a negative adjustment to the rate based on the lower risk.

How does lock period influence a home loan interest rate?

When a loan originator quotes you an interest rate, it is based on the market at the time that they are quoting you the rate. That rate can rise or fall during the process of document collection and underwriting. To stabilize the rate and give real numbers to the lender and the borrower (you), the originator will lock the rate for a period that they estimate will get the borrower to closing. The longer the period of the lock, the higher the adjustment to the interest rate. For example, a 30-day lock may cost -0.17 and a 60-day lock may cost 0.13.

What are lender credits and how do they affect a home loan interest rate?

Lender credits are generally offered as a promotion (or sale) that the lender is having. For example, in order to entice borrowers to refinance, they may have a promotion to give a half point (-0.5) credit towards the rate on all refinance loans for a specific period. This means that any loan locked within their promotion period, will have this credit applied and the savings will be returned to the borrower in terms of a lower percentage rate. This is out of the control of the borrower as there is no indication of when a lender will release a promotional credit. Lender credits can also be given for accepting a higher interest rate and can be used to cover closing costs. This is out of the scope of this article, but will be covered in the future.

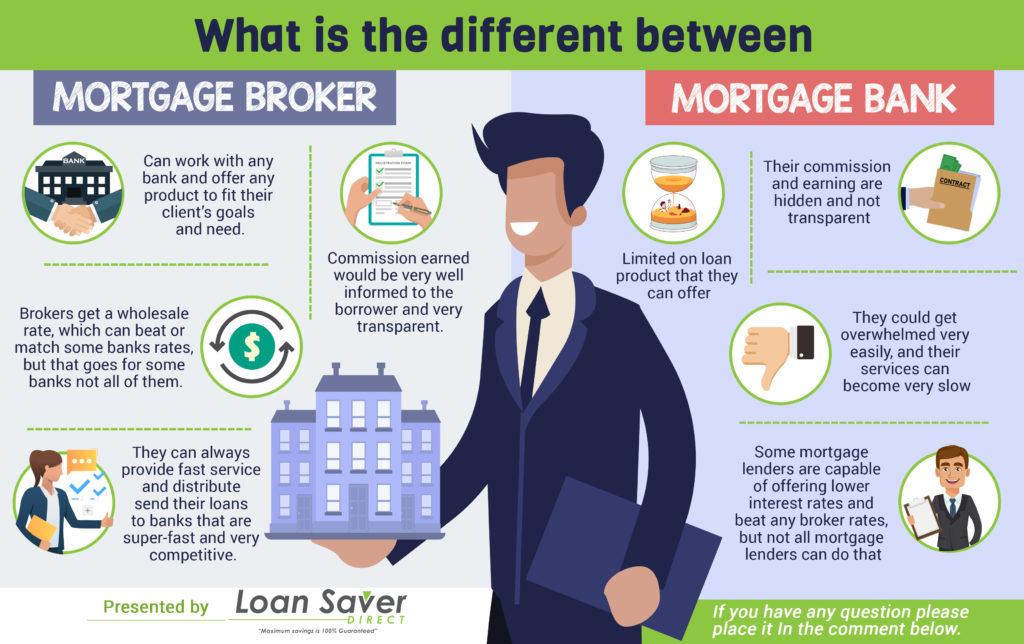

Will a lender or broker be able to offer a better home loan interest rate?

This seems to be a widely-asked question. Brokers are given wholesale prices for rates that borrowers do not have access to. Furthermore, brokers have access to multiple lenders, within their network, to shop rates for a particular home loan scenario and find the best interest rate for the buyer (you). Rates vary from lender to lender for different products. For example, Lender A may have great VA rates, however higher conventional rates. Lender B may have great rates for conventional but lacking for FHA. Lender C may have great FHA rates but the rates for Conventional and VA are higher.